- Compute and journalize bad debt expense under the allowance method (percentage of sales)

GAAP requires companies to match expenses to revenue as closely as possible. Under the direct write-off method of accounting for uncollectible accounts receivable, you could have revenue in October, finish the year, and report that revenue to investors and creditors, and then in the next year, find that account has gone bad. As accountants, we don’t want to go back to the prior year, change it, restate it, and publish new financials. That would be time-consuming and the users of those financials would be frustrated if we were always going back and changing the financials. So, once a year is over, and the books are closed, it’s done and we don’t go back.

What are the other alternatives? The FASB asked this question and the answer that came back was this: if we (accountants) could reasonably estimate bad debts in some way we could post an expense in the same year or other time period as the revenue/receivable was booked.

The easiest, but least accurate way to do this is to simply take a percentage of sales, based on a historical average, and use it as an estimate, and then periodically make sure it is fairly accurate over time. We call this the percentage-of-sales method. Also, sometimes accountants refer to this method as the income statement method because the focus is on the expense account.

The formula to estimate bad debts expense is:

Bad debt expense = Net sales (total or credit) × Percentage estimated as uncollectible

Technically, we should base bad debt expense on credit sales only, but if cash sales are small or make up a fairly constant percentage of total sales, bad debt expense could be based on total net sales. Since at least one of these conditions is usually met, companies commonly use total net sales rather than credit sales.

Here’s an example. Larkin Co. is a start-up accounting firm that billed out $1 million in services during the year (a) and collected $750 thousand of that revenue (b):

While preparing the year-end financial statements before the close of the year, Larkin Co. decides to use the percentage-of-sales method to estimate a reduction to sales that will closely approximate the revenue they have booked that they will never actually collect. They are using the same credit policies as other accounting firms and expect about the same amount of bad debt on a percentage basis. They use an industry standard (that one of the experienced partners in the firm has provided) of 1%.

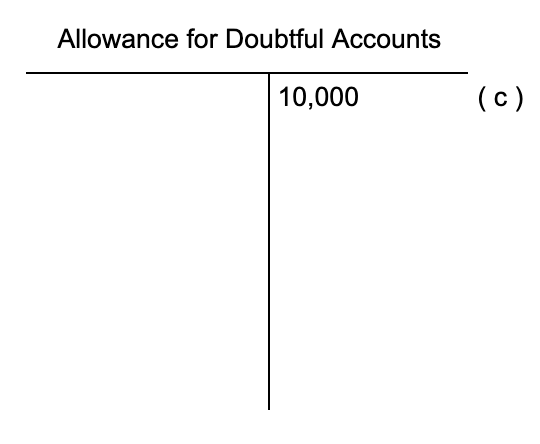

Based on this percentage, the amount of revenues that will never be collected is 1,000,000 × .01 = $10,000.

So, they make this entry (c):

| Date | Description | Post. Ref. | Debit | Credit |

|---|---|---|---|---|

| 20– | ||||

| Dec 31 | Bad Debt Expense | 10,000.00 | ||

| Dec 31 | Allowance for Doubtful Accounts | 10,000.00 | ||

| Dec 31 | To record bad debts as a percentage of sales |

We post this entry to the GL:

Notice they did not post the credit side of the entry to Accounts Receivable because the subsidiary account always, always, always has to agree with the control account. They could create a fictitious customer in the subsidiary ledger and then post the credit to the fictitious customer’s account, but it’s not common practice to do that. Instead, we create a separate GL account called Allowance for Doubtful Accounts. It’s a companion account to Accounts Receivable, and since it has a credit balance, it is called a “contra account.” We’ll see more of these acoounts as we go on.

Here is what the GL looks like now:

Bad Debt Expense is not considered a contra account to Revenue. It’s a stand-alone account usually classified as a selling expense (which you will see in the module on Merchandising Operations). However, Allowance for Doubtful Accounts is attached to Accounts Receivable. It holds the amount we have determined is uncollectible until we actually identify the accounts that go bad.

You can see from these few T accounts that although total gross revenues are $1 million, we have created a matching expense that records the estimated amount that will be uncollectible. The matching principle requires us to book expenses in the same period as the revenues to which they are related to the best of our ability.

Also, we now have a net number for accounts receivable. The net receivable, adjusted for the estimated uncollectible accounts is $750,000 (gross receivables) minus the allowance of $10,000. That means that we expect to collect in cash $740,000 once all the payments and non-payments are accounted for. Accountants call this collection the net realizable value. Remember, to recognize a revenue or an expense means to record it, and to realize it means it actually happens. In this case, to realize a revenue recorded “on account” means to collect the cash.

If you wanted to sell all your receivables to me (called “factoring”), I would not buy them from you based on the gross amount, which is both the control account and the detailed list of customers from whom I will collect (the subsidiary ledger). I would buy them from you based on the net realizable value—the cash I would expect to ultimately collect. We’ll cover factoring in slightly more detail a bit later.

Accounts Receivable and its companion account, Allowance for Doubtful Accounts, are permanent accounts and are not closed at the end of the accounting cycle. Revenues and Bad Debt Expense are temporary accounts and are closed to capital at the end of the cycle. So, in year two, the beginning balances of Larkin Co. look like this:

Assume the subsidiary receivables ledger looks something like this (simplified):

| Customer | Amount Owed |

|---|---|

| A | 57,500 |

| B | 22,000 |

| C | 74,500 |

| D | 8,000 |

| E | 12,500 |

| F | 25,000 |

| G | 50,500Single line |

| 250,000Double line | |

Notice how the subsidiary ledger agrees to the GL control account and does not include our estimated $10,000 of bad debt.

Now, in year 2, client D refuses to pay and then disappears. All efforts to collect fail. In February, we decide to write off the account as a loss.

| Date | Description | Post. Ref. | Debit | Credit |

|---|---|---|---|---|

| 20– | ||||

| Feb 28 | Allowance for Doubtful Accounts | 8,000.00 | ||

| Feb 28 | Accounts Receivable | 8,000.00 | ||

| Feb 28 | To write off bad account from client D |

We post this entry to both the GL and the subsidiary ledger:

The subsidiary ledger agrees with the control account.

| Customer | Amount Owed |

|---|---|

| A | 57,500 |

| B | 22,000 |

| C | 74,500 |

| D | |

| E | 12,500 |

| F | 25,000 |

| G | 50,500Single line |

| 242,000Double line |

We haven’t posted any other transactions, but you can see we didn’t record the write off of the prior year’s sale as an expense in this year. We already “recognized” the expense in year one when we recognized the revenue from all that work we did. This year, we are simply recognizing the actual account that went bad. (Assume all those others are paying or have paid. Now there are new revenues and new accounts receivable, but right now we’re just trying to isolate this one issue).

Think of the allowance for doubtful accounts as a place to hold “accounts that will go bad in the future, we just don’t know which account that is yet.” When we actually identify the account(s) that go bad, we remove that account from the subsidiary ledger and the GL by moving from the “unidentified” bad accounts to the actual lists (control and subsidiary).

Notice three things:

- Bad Debt Expense is recognized in the same period that the revenue is recognized.

- The estimate ($10,000 in this case) may not be exact. We are balancing the matching principle and usefulness against perfection. We don’t need to be perfectly accurate. We need to provide a reasonable picture of the company’s financial position at the end of the year, and that includes an estimate of accounts that will never materialize into cash.

In applying the percentage-of-sales method, companies annually review the percentage of uncollectible accounts that resulted from the previous year’s sales. If the percentage rate is still valid, the company makes no change. However, if the situation has changed significantly, the company increases or decreases the percentage rate to reflect the changed condition. For example, in periods of recession and high unemployment, a firm may increase the percentage rate to reflect the customers’ decreased ability to pay. However, if the company adopts a more stringent credit policy, it may have to decrease the percentage rate because the company would expect fewer uncollectible accounts.

Again, this “income statement method” is the easiest to apply, but not the most accurate. In fact, it is not considered GAAP, so public companies who file audited financial statements with the SEC cannot use this method. We’ll cover a better method, the one used by most companies for year end financials, in the next section.