- Evaluate the pros and cons of renting and homeownership

- Calculate the monthly payment and interest expenses of a mortgage

- Interpret and understand an amortization schedule

Homeownership Versus Renting

You can view the transcript for “Do you know what are the Pros and Cons of Renting vs Buying” here (opens in new window).

Understanding and Calculating Mortgage Payments

The Main Idea

A mortgage is a type of loan, typically used to purchase a home, where the property serves as the collateral. The mortgage payment comprises principal repayment and interest payment. The interest is the cost of borrowing the principal amount for the purchase.

To calculate the monthly payment of a mortgage, you need to know the principal amount (the loan amount), the interest rate, and the loan term. The formula to calculate the monthly payment (PMT) on a mortgage is as follows:

where [latex]PMT[/latex] is the monthly mortgage payment, [latex]P[/latex] is the principal loan amount, [latex]r[/latex] is the annual interest rate in decimal form and [latex]t[/latex] is the number of years of the payment.

To find the total amount of your payments over the life of the loan, multiply your monthly payments by the number of payments. The total paid, [latex]T[/latex], on an [latex]t[/latex] year mortgage with monthly payments [latex]pmt[/latex] is [latex]T=pmt\times12\times t[/latex].

The cost of financing a mortgage, [latex]CoF[/latex], is [latex]CoF=T−P[/latex] where [latex]P[/latex] is the mortgage’s starting principal and [latex]T[/latex] is the total paid over the life of the mortgage.

Escrow Payments

The Main Idea

An escrow account is a type of account that your mortgage lender sets up on your behalf when you close on your home. This account is used to pay certain property-related expenses on your behalf. The most common expenses that are paid out of an escrow account are property taxes and homeowners insurance. When you take out a mortgage, the lender typically divides the estimated annual cost of these expenses by [latex]12[/latex] to determine a monthly amount. You then pay this amount as part of your monthly mortgage payment. The lender deposits these funds into the escrow account and then pays the expenses out of the account as they come due. This spreads out the cost of these large expenses into manageable monthly payments and ensures that these important bills are paid on time.

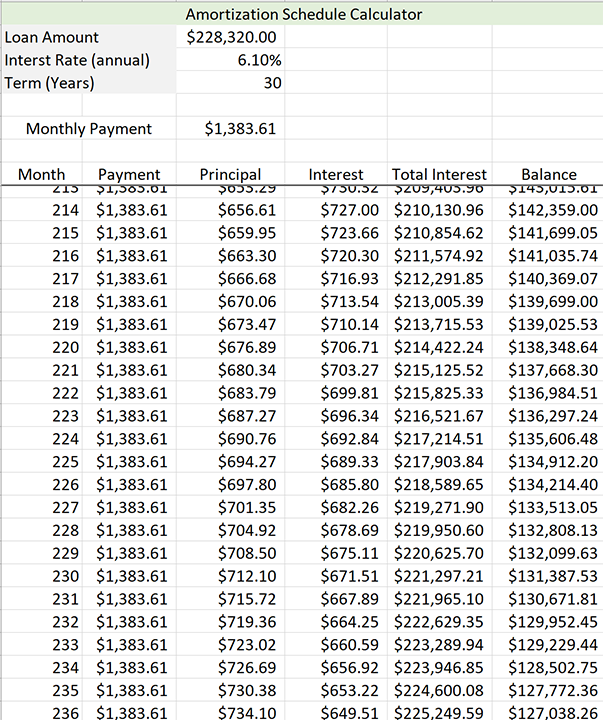

Reading and Interpreting Amortization Tables

You can view the transcript for “Amortization Schedule Explained” here (opens in new window).

- What is the interest rate?

- How much are the payments?

- How much of payment [latex]235[/latex] goes to principal?

- How much of payment [latex]215[/latex] goes to interest?

- What’s the remaining balance on the mortgage after payment [latex]227[/latex]?

- At what payment does the amount that is applied to mortgage finally exceed the amount applied to interest?