Who Uses Financial Reports?

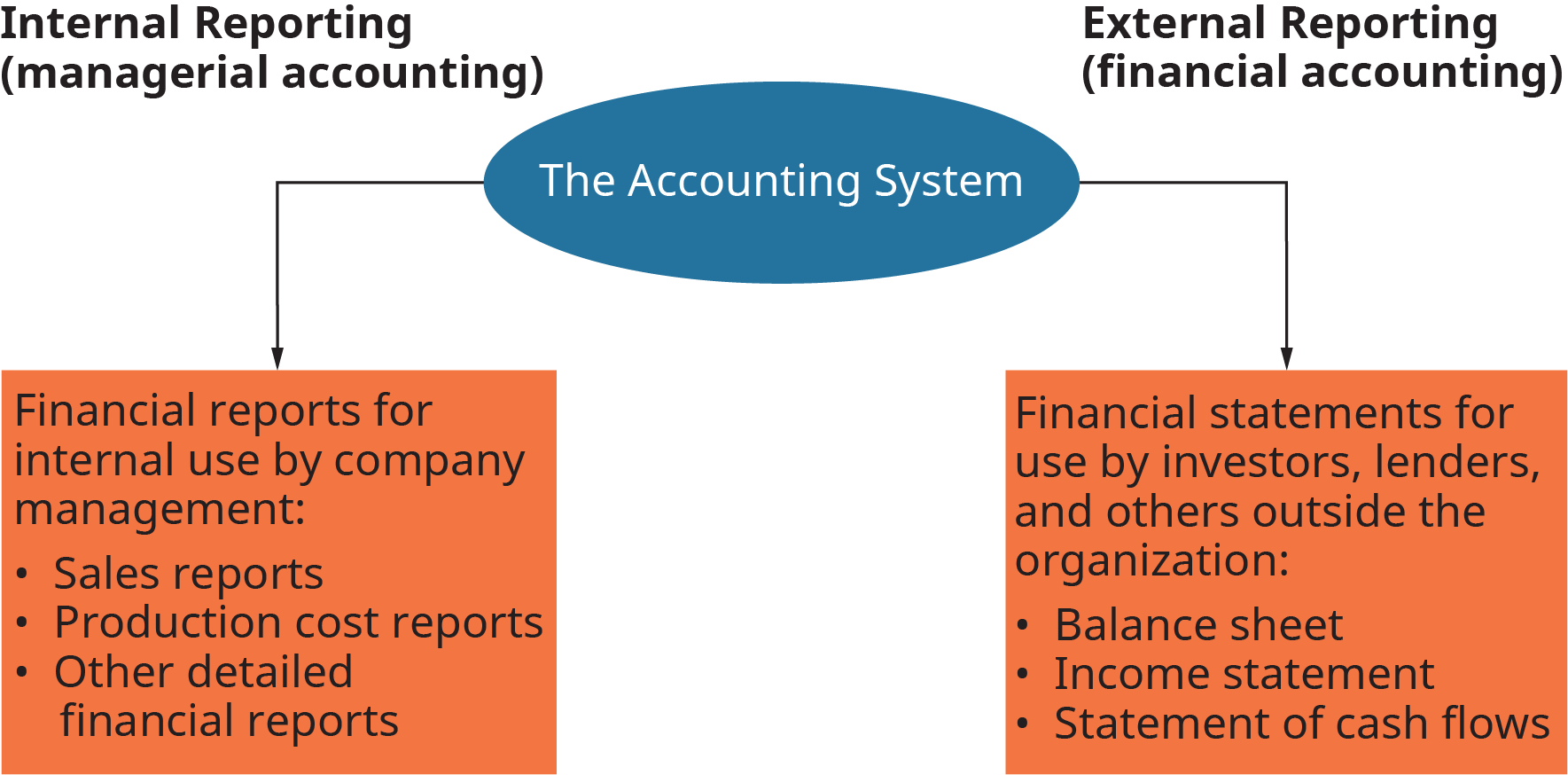

The accounting system generates two types of financial reports, as shown above: internal and external. Internal reports are used within the organization.

Managerial Accounting

As the term implies, managerial accounting provides financial information that managers inside the organization can use to evaluate and make decisions about current and future operations. For instance, the sales reports prepared by managerial accountants show how well marketing strategies are working, as well as the number of units sold in a specific period of time. This information can be used by a variety of managers within the company in operations as well as in production or manufacturing to plan future work based on current financial data. Production cost reports can help departments track and control costs, as well as zero in on the amount of labor needed to produce goods or services. In addition, managers may prepare very detailed financial reports for their own use and provide summary reports to top management, providing key executives with a “snapshot” of business operations in a specific timeframe.

Financial Accounting

Financial accounting focuses on preparing external financial reports that are used by outsiders; that is, people who have an interest in the business but are not part of the company’s management. Although they provide useful information for managers, these reports are used primarily by lenders, suppliers, investors, government agencies, and others to assess the financial strength of a business.

Note that both managerial and financial accounting involve preparing financial reports, but only in financial accounting do you prepare financial statements.

Accounting Standards

To ensure accuracy and consistency in the way financial information is reported, accountants in the United States must follow generally accepted accounting principles (GAAP) when statements are prepared for financial accounting. The Financial Accounting Standards Board (FASB) is a private organization that is responsible for establishing financial accounting standards used in the United States. In contrast, the statements for managerial accounting can be changed and presented based on the needs of management.

Currently there are no international accounting standards. Because accounting practices vary from country to country, a multinational company must make sure that its financial statements conform to both its own country’s accounting standards as well as the standards of any other country where they conduct business. Often another country’s standards are quite different from U.S. GAAP. In the past, the U.S. Financial Accounting Standards Board and the International Accounting Standards Board (IASB) worked together to develop global accounting standards that would make it easier to compare financial statements of foreign-based companies. However, as of this writing, the two organizations have not agreed on a global set of accounting standards.

What’s It Like to Be an Accountant?

You can view the transcript for “Pros & Cons of Being an Accountant | Salary, Work-life balance, & Q&A” here (opens in new window).