- Understand what accounting is

- Understand who uses financial accounting

- Understand who uses managerial accounting

Why Do We Need Financial Information?

In the same way that you track your monthly spending, businesses have large groups of stakeholders who have a vested interest in the continued success of the enterprise. If a business, whether for-profit or nonprofit, becomes financially insolvent and can’t pay its bills, it will be forced to close. Financial information enables a business to track its accounts and make informed financial decisions.

Each business needs financial information to be able to answer questions such as the following:

- How much cash does the business need to pay its bills and employees?

- Is the business profitable, earning more income than it pays in expenses, or is it losing money and possibly in danger of closing?

- How much of a particular product or mixture of products should the business produce and sell?

- What is the cost of making the goods or providing the service?

- What are the business’s daily, monthly, and annual expenses?

- Do customers owe money to the business, and are they paying on time?

- How much money does the business owe to vendors (suppliers), banks, or other investors?

What Is Accounting?

Accounting is the process of collecting, recording, classifying, summarizing, reporting, and analyzing financial activities. It results in reports that tell the financial story of the organization. All types of organizations—businesses, hospitals, schools, government agencies, and civic groups—use accounting procedures. Accounting provides a framework for looking at past performance, current financial health, and possible future performance. It also provides a framework for comparing the financial positions and financial performances of different firms. Understanding how to prepare and interpret financial reports will enable you to evaluate two companies and choose the one that is more likely to be a good investment.

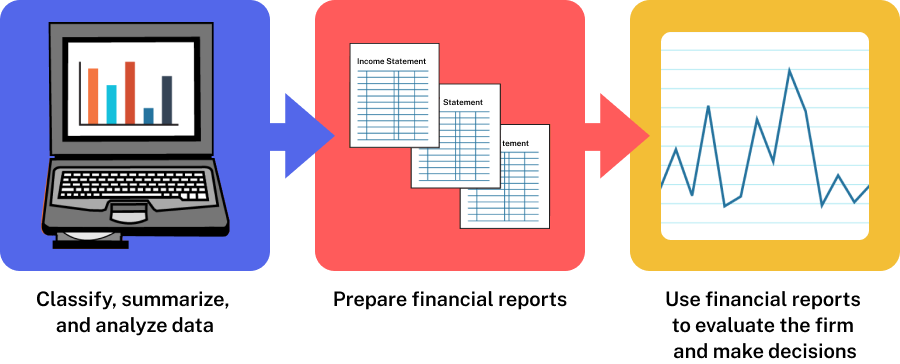

The accounting system shown below converts the details of financial transactions (sales, payments, purchases, and so on) into a form that people can use to evaluate the firm and make decisions. Data become information, which in turn becomes reports. These reports describe a firm’s financial position at one point in time and its financial performance during a specified period. Financial reports include financial statements, such as balance sheets and income statements, and special reports, such as sales and expense breakdowns by product line.

Bookkeeping vs. Accounting

Accounting is often confused with bookkeeping. Bookkeeping is the manual or electronic process of recording the financial transactions of a business. Accounting includes bookkeeping, but it goes further to analyze and interpret financial information, prepare financial statements, conduct audits, design accounting systems, prepare special business and financial studies, prepare forecasts and budgets, and provide tax services.