Structure/Organization of the Federal Reserve System

The organization responsible for conducting monetary policy and ensuring that a nation’s financial system operates smoothly is called the central bank. Most nations have central banks or currency boards. Some prominent central banks around the world include the European Central Bank, the Bank of Japan, and the Bank of England. In the United States, the central bank is called the Federal Reserve—often abbreviated as “the Fed.” This section explains the organization of the U.S. Federal Reserve and identifies the major responsibilities of a central bank.

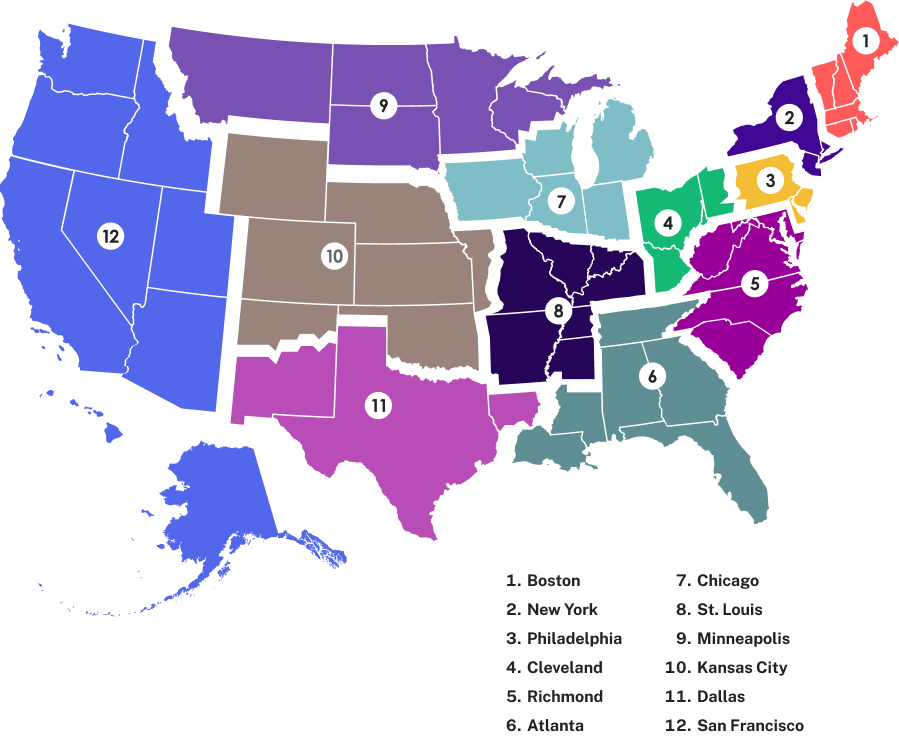

The Fed’s primary mission is to oversee the nation’s monetary and credit system and to support the ongoing operation of America’s private-banking system. The Fed’s actions affect the interest rates banks charge businesses and consumers, help keep inflation under control, and ultimately stabilize the U.S. financial system. The Fed operates as an independent government entity. It derives its authority from Congress but its decisions do not have to be approved by the president, Congress, or any other government branch. However, Congress does periodically review the Fed’s activities, and the Fed must work within the economic framework established by the government. The Fed consists of 12 district banks, each covering a specific geographic area. Each district has its own bank president who oversees operations within that district.

What Does the Fed Do?

Originally, the Federal Reserve System was created to control the money supply, act as a borrowing source for banks, hold the deposits of member banks, and supervise banking practices. Its activities have since broadened, making it the most powerful financial institution in the United States.

Functions of the Federal Reserve

The Federal Reserve, like most central banks, is designed to perform the following three important functions:

- To conduct monetary policy

- To promote stability of the financial system

- To provide banking services to commercial banks and other depository institutions, and to provide banking services to the federal government

The Federal Reserve provides many of the same services to banks as banks provide to their customers. For example, all commercial banks have an account at the Fed where they deposit reserves, and they can obtain loans from the Fed.

Check Processing

The Fed is also responsible for check processing. When you write a check to buy groceries, for example, the grocery store deposits the check in its bank account. Then, the physical check (or an image of that actual check) is returned to your bank, after which funds are transferred from your bank account to the account of the grocery store. The Fed is responsible for how these transactions are handled once the check leaves the cash register and is deposited into the store’s bank account. Does that mean that your check to the grocery store goes all the way to Washington, DC.? No. Instead, the regulations that govern how banks handle checks, deposits, and withdrawals are regulated by The Federal Reserve Act. This act is the reason that a bank must start paying you interest on a savings deposit the day it is received. It’s also the reason that if you deposit a large check, your bank may tell you that the funds will not be available for three to five business days.

Money in Circulation

The Federal Reserve also ensures that enough currency and coins are circulating through the financial system to meet public demands. For example, each year, the Fed increases the amount of currency available in banks around the holiday shopping season at the end of the year and reduces it again in January.

Legal Compliance

Finally, the Fed is responsible for assuring that banks are in compliance with a wide variety of consumer protection laws. For example, banks are forbidden from discriminating on the basis of age, race, sex, or marital status. Banks are also required to publicly disclose information about the loans they make for buying houses and how those loans are distributed geographically, as well as by sex and race of the loan applicants.